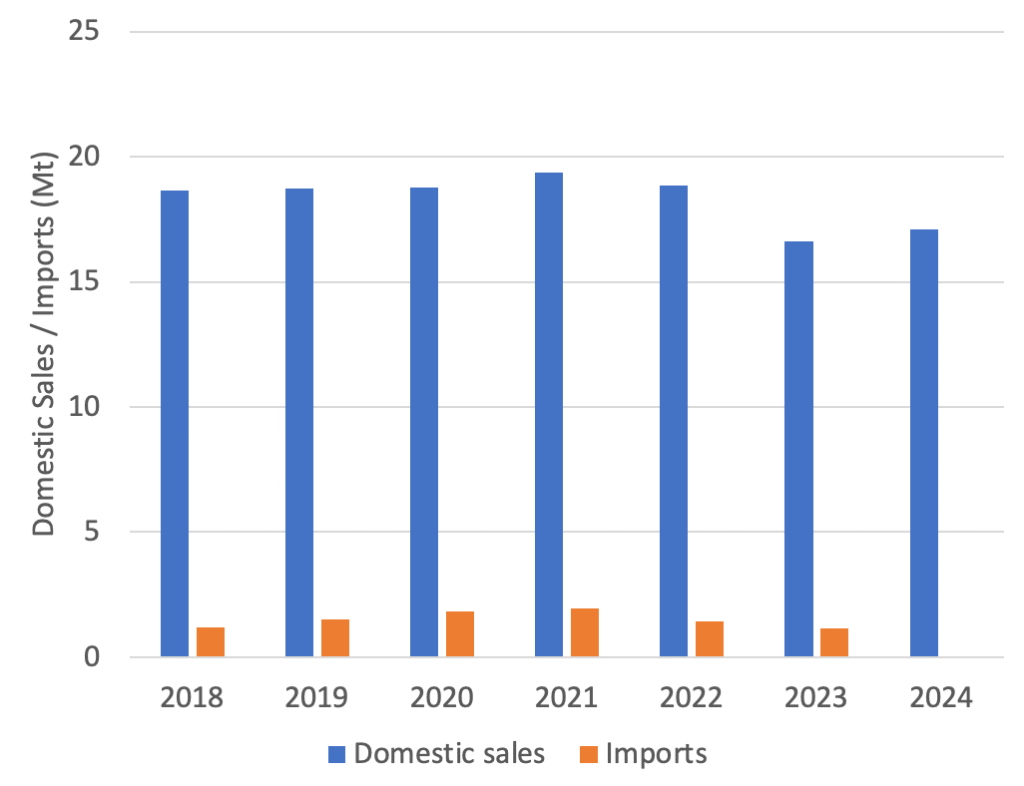

The European cement industry, particularly in Poland, is grappling with significant challenges. A substantial influx of cement imports from non-EU countries, notably Ukraine, has intensified competition. These imports have surged by nearly 3,000% over five years, reaching over 650,000 tonnes in 2024, with projections exceeding 1 million tonnes in 2025 . This surge is attributed to Ukrainian producers not bearing the costs associated with the EU’s stringent climate policies, such as the Emissions Trading Scheme (ETS), giving them a competitive edge .POLITICO+1GlobeNewswire+1Бизнес PAP+1cementintel.com+1

In response, the Polish Cement Association (SPC) has raised concerns about the viability of domestic cement production, citing high energy prices, decarbonization costs, and the threat of carbon leakage. The SPC has called for measures like customs quotas on Ukrainian cement imports and the extension of the EU ETS indirect cost compensation scheme to include the cement sector .

The Role of Slag in Sustainable Construction

Amid these challenges, slag—a byproduct of steel production—has emerged as a sustainable alternative in the construction industry. In 2023, 29.7 million tonnes of slag were utilized in building materials across the EU and the UK. Of this, 20.3 million tonnes were granulated blast furnace slag, with 18.3 million tonnes ground for use in cement production . The use of slag not only conserves natural resources by substituting limestone and clay in clinker production but also significantly reduces CO₂ emissions, aligning with the EU’s decarbonization goals.Global Concrete

Opportunities for Slag Suppliers

The current landscape presents a unique opportunity for companies specializing in slag supply. As the EU pushes for greener construction materials, the demand for slag as a supplementary cementitious material is poised to grow. By providing high-quality slag, suppliers can support the cement industry’s transition towards sustainability, helping to mitigate the environmental impact of construction while also addressing the challenges posed by non-EU imports.

Conclusion

The European cement industry’s current challenges underscore the need for sustainable alternatives. Slag offers a viable solution, contributing to resource conservation and emission reductions. For slag suppliers, this represents not only a business opportunity but also a chance to play a pivotal role in the EU’s journey towards sustainable construction.